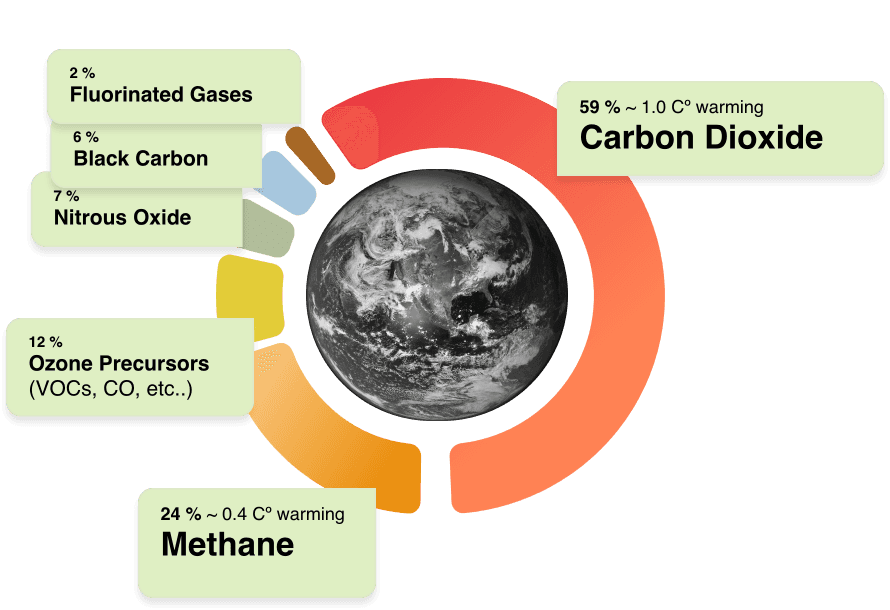

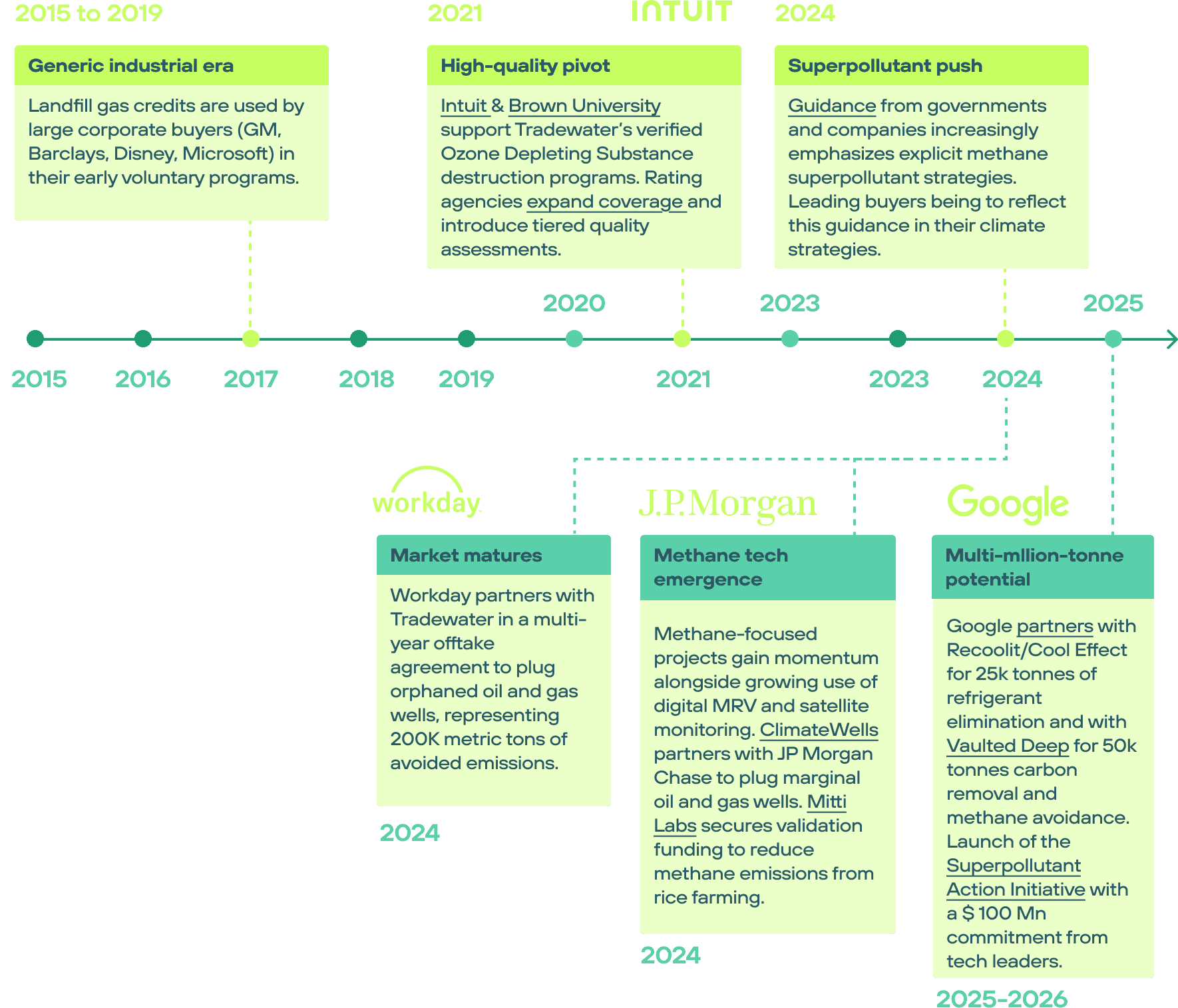

The other half of global warming

The UNEP’s Climate and Clean Air Coalition defines superpollutants as: ‘’a group of atmospheric pollutants that have greater impacts on warming than carbon dioxide per tonne, and can have other environmental and human health effects.’’

Superpollutant gases include: methane, tropospheric ozone and its precursors, fluorinated gases (F-gases and Hydrofluorocarbons), nitrous oxide, and black carbon. These gases are emitted across a range of sectors, such as energy generation, industrial processes, agriculture, waste, and the built environment.

Collectively, this family of greenhouse gases (GHG) is responsible for close to 50% of today’s warming. Yet, unlike carbon dioxide (CO₂), the urgent need to reduce their emissions remains overlooked, both in public discourse and in funding priorities.

The climate impact of superpollutants

Source: IPCC AR6 WGI SPM Fig 2c (2021)

Note: Historical warming to date - Sum of percentages > 100% due to cooling effect from aerosols and land use change.

Superpollutants: where do they come from?

Methane

GHG

Agriculture (livestock, rice cultivation, manure management), fossil fuels (extraction, processing, distribution of oil, gas and coal), waste (landfills, wastewater treatment)

Troposph. ozone

GHG & air pollutant

Tropospheric ozone is not directly emitted. It is a secondary pollutant formed by the reaction of precursor gases (such as methane, nitrogen oxide, carbon monoxide, and volatile organic compounds) in the presence of sunlight. Sources of precursors include vehicle exhaust and industrial emissions.

Nitrous oxide

GHG

Agriculture (nitrogen-based fertilizers), industrial processes (nitric and adipic acid for nylon production), fossil fuels (combustion), waste (wastewater treatment)

Black carbon (Soot)

Particulate matter

Incomplete combustion of fossil fuels, biofuels, & biomass (wildfires, agricultural burning, cooking with coal, wood, kerosene, diesel engine, residential heating, waste burning)

Hydrofluo-rocarbons (HFCs)

GHG

Man-made chemicals used primarily as refrigerants in air conditioning and refrigeration, as well as aerosol propellants, solvents and foam-blowing agents

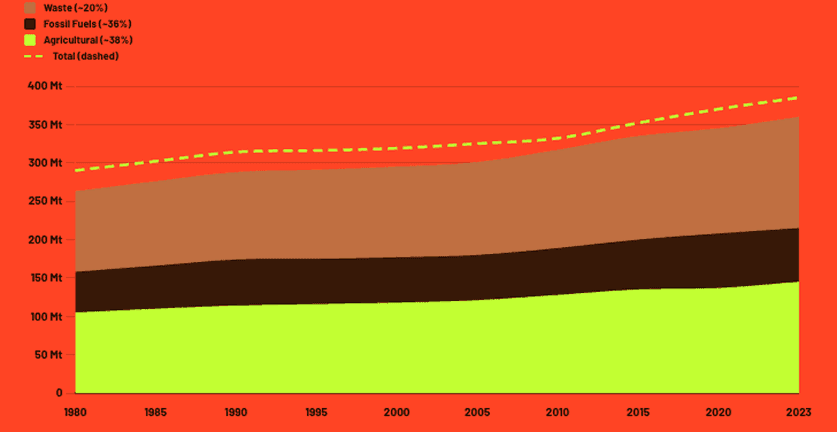

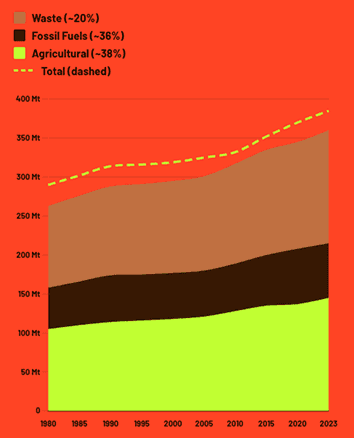

Methane matters: why emissions are rising

For the last decade, emissions of superpollutants and methane in particular, have continued to rise. This trend is driven in part by growing methane emissions from agriculture.

“Methane’s atmospheric concentrations have more than doubled since pre-industrial times. According to new modelling, global anthropogenic emissions of methane reached approximately 352 million tonnes (Mt) per year in 2020 and, under current legislation, are projected to continue rising, reaching 369 Mt per year in 2030, 5% above 2020.’’

Source: Spark Climate Solutions / EDGAR / Global Carbon Project / IPCC AR6

Agriculture is the largest source of anthropogenic methane emissions

Agriculture

Livestock

Produced in the stomachs of ruminants (cows, sheep) during digestion and released via belching

Agriculture

Rice cultivation

Flooded paddies create low-oxygen soil conditions where methane-producing bacteria thrive.

Agriculture

Manure

Decomposition of animal waste, specifically when stored in liquid lagoons or tanks.

Fossil Fuels

Oil & gas operations

Fugitive leaks from pipelines, intentional venting at wells, incomplete flaring, or abandoned mines.

Fossil Fuels

Coal mining

Methane trapped inside coal seams is released during extraction (or when mines are abandoned).

Waste

Landfills

Food and organic waste buried underground rots without oxygen (anaerobic decomposition).

Waste

Waste water treatment

Breakdown of sewage and industrial organic matter in treatment plants.

Other

Biomass burning

Incomplete combustion during large-scale burning of forests or crop residues.

High-impact but short-lived

In addition to their outsized impact on the climate, superpollutants have the particularity of decomposing over short periods of time, ranging from a few days to a few years. In contrast, CO₂ has a longer lifetime and tends to accumulate in the atmosphere.

To quantify the difference between this ‘’flow’’ (superpollutants) and ‘’stock’’ (CO₂) behaviors, scientists have developed a useful framework around the concept of ‘’Global Warming Potential’’ (GWP). GWP is a metric used to compare how much heat is trapped by different greenhouse gases over a specific period of time. This metric captures both the ‘’radiative forcing’’ (eg. how much heat can be trapped by a gas) and its atmospheric lifetime.

GWP allows us to quantify the climate impact of different super pollutant gases through a common unit: carbon dioxide-equivalent (CO₂e). This represents a first step on the path to scaling the abatement of superpollutants, which must run as a parallel track to reducing CO₂ emissions.

Crucially, GWP can be expressed in 100 or 20-year time frames, with the latter being the most useful for reflecting the rapidly decaying properties of these gases.

In this table, the GWP20 column helps us visualize why superpollutants are a major source of historical warming. Scientific consensus is now clear around the need to rapidly abate their emissions in order to contain future warming.

The impact of superpollutants is stronger on the short term

Methane

~12 Years

85

28

Tropospheric ozone

Hours to weeks

N/A*

N/A*

Nitrous oxide

~ 109 Years

273

273

Black carbon (Soot)**

Days to weeks

1,600

273

Hydrofluo-rocarbons (HFCs)

1 to 270 years

Hundreds to tens of thousands***

Hundreds to tens of thousands

*A secondary pollutant without a direct source. Its warming effect is covered by the GWP of is precursor gases, primarily methane.

**GWP is less appropriate for aerosols, and values are highly uncertain. Black carbon causes rapid, localized warming

*** Values vary drastically by compound. For example, R-410A, widely used in air conditioning has a GWP100 around 2,256.

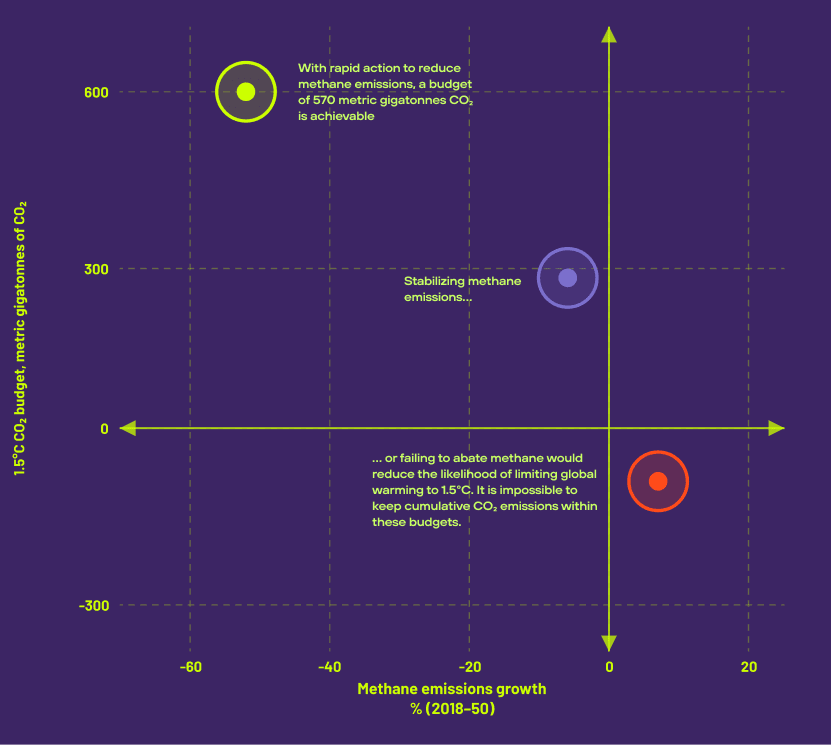

Impact of methane emissions scenarios on the remaining 1.5°C CO₂ budget

Source: McKinsey Sustainability

The race to stay

under 1.5°C

Scientific consensus is now clear around the need to rapidly reduce superpollutant emissions in order to contain future warming. Superpollutant abatement does not lessen the need to cut carbon dioxide, an essential pillar of long-term climate stability.

However, as the world enters what the IPCC describes as a “danger zone” for near-term warming and climate risk, it becomes critical to pair long-term decarbonization with fast-acting strategies that curb immediate damage.

To avoid crossing irreversible tipping points and stay within the Paris Agreement warming boundaries, the Carbon Containment Lab's mission outlines a dual strategy:

A. the sprint to 2030: cut emissions of superpolllutants

B. the marathon to 2050: achieve long term decarbonization

“Action taken on superpollutants now will deliver near-term warming mitigation within decades, not centuries.’’

Justin Freiberg

Managing Director,

Carbon Containment Lab (CC Lab)

“Studies suggest that mitigating the entire stock of superpollutants could avoid more than half a degree Celsius of warming by mid-century and over one degree by the end of the century. Investing in superpollutant mitigation may be among the best uses of climate capital today.’’

Superpollutants, tackling a major threat - Calyx Global & CC Lab

Methane

0.2°C of warming can be avoided by 2050 by mitigating just 30% of the 11 billion MTCO2e GWP100 of methane emitted annually.

Improvements in local air quality. In rice cultivation, Climate-smart irrigation techniques like AWD generate substantial savings in water usage (40%).

Tropospheric ozone

N/A

N/A

Nitrous oxide

0.2°C of warming can be avoided by 2050 by cutting emissions by 50-75%

Ozone layer protection. Improvement in air quality. More precise use of fertilizers improves water quality

Black carbon

Improvements in local air quality

Hydrofluo-rocarbons (HFCs)

0.5°C of warming can be avoided by 2100 by achieving complete international compliance with the Kigali Amendment to the Montreal protocol

Improvements in local air quality

Source: Calyx & Carbon Containment Lab

On the policy side, there are renewed efforts to incentivize and mandate the abatement of superpollutants and of methane in particular. Some examples include: The Global Methane Pledge (signed by 150 countries), the Methane Emissions Reduction Program, the Waste Emissions Charge in the United States, and the European Union’s Methane Regulation which prohibits methane flaring in the energy sector. For a full view of methane-specific policies, visit this useful explorer from Climate Analytics.

The Kigali Amendment to the Montreal Protocol phases down the production of high GWP HFC gases used for cooling, and is already taking effect.

On the co-benefit side, and because many superpollutants are also air pollutants, reducing their presence in the atmosphere will lead to better health and food security outcomes.

“By midcentury, reducing superpollutants could prevent millions of premature deaths annually and save tens of millions of tonnes of crops annually, by improving air quality through reductions in both superpollutants and their co-emissions’’

CCAC - UNEP

Why this platform?

This platform was created following a 2025 New York Climate Week co-organized by Mitti Labs and the Carbon Containment Lab. It gives an overview of the state of the field, with key definitions and metrics, case studies of superpollutant projects, discussion of carbon finance trends, and links to online resources.

Our aim with this platform is to educate and inspire action from the private sector, alongside continued improvement in policies. Markets that support superpollutant abatement are still developing, and the organizations that are supporting and funding this work are diverse and growing.

Looking at climate finance as a whole helps bring into focus the urgency for action: Pollutants responsible for almost half of today’s warming receive less than 5% of climate funding.

The critical question is: can the right incentives in voluntary carbon markets (VCMs) and corporate offsetting help close this finance gap and catalyze large-scale action on superpollutant abatement?

About us

Mitti Labs combines satellite technology, Artificial Intelligence and operations on the ground to permanently reduce methane emissions from rice farming. By doing this, the company unlocks the potential of rice-based carbon credits for climate impact at scale. Mitti Labs is backed by Lightspeed, Voyager Ventures, Cisco, and Volta Circle in its mission to decarbonize the $300 billion rice-growing industry worldwide. Visit mittilabs.earth to learn more.

“When we started Mitti Labs it was hard to access information on the market for methane-based carbon credits. There was little data on what methodologies to follow, how to price our credits, or successful strategies to market them. 2026 will be a watershed year in unleashing the potential of ‘Beyond CO₂’ credits to deliver real climate impact. We want to encourage a wide sharing of knowledge within the ecosystem to accelerate this impact.’’

Xavi Laguarta

Co-founder, Mitti Labs

The growing market for superpollutant

credits

The market for superpollutant mitigation is already emerging. From orphan well plugging to refrigerant destruction and interventions in rice farming, project developers are deploying technologies that cut some of the most powerful warming gases in the atmosphere. This is happening today, at scale, and at relatively low cost.

These efforts operate within the broader carbon credit ecosystem: methodologies set the rules for measuring impact, registries issue and track credits, and independent rating agencies evaluate quality. Together, they transform measurable emissions reductions into investable climate assets, allowing capital to flow where it is needed most.

Early participants have demonstrated that the underlying technologies work and that measurement is often more straightforward than in other credit categories. What's still missing is simple: clearer guidance for buyers, stronger quality signals, and the financial architecture to move from niche to norm.

02 | Building the market: insights from early movers

The climate opportunity

Dean Takahashi

Executive Director, Carbon Containment Lab

The following sections dive into the ‘’supply’’ side of the market for superpollutant-based credits. These are project developers working to abate or mitigate superpollutant emissions across project types and geographies. These projects trace the way forward in mobilizing market forces for large-scale abatement.

Project Drawdown has developed a useful directory of ‘’Climate Solutions’’. For a deep dive into superpollutant-specific solutions, consult: Improve rice production, Deploy alternative refrigerants, Improve refrigerant management, Manage oil & gas methane

The carbon credit ecosystem

Just like carbon-based projects, a superpollutant abatement project must navigate a structured ecosystem of rules, oversight, and verification in order to generate a carbon credit. What follows is a map of that ecosystem.

Methodologies are the rulebooks. For project developers, they are the bridge between deploying a technology to abate or mitigate the emission of a superpollutant and building the economic viability to scale this intervention.

The Carbon Containment Lab has provided a useful count of superpollutant-specific methodologies, with breakdown by superpollutant type. They define the role of methodologies as follows:

“Methodologies are issued by registries and follow common standard-setting procedures to be developed, including peer review and public comment (…) Methodologies describe the measurement, verification, and reporting activities that are required to determine whether a project can be eligible to sell a tradable credit for the activity type that the methodology covers. All told, methodologies are key tools that define the volume and quality of carbon credits being issued.”

Anastasia O'Rourke

Senior Managing Director, Carbon Containment Lab

Active superpollutant methodologies

Number

81

21

19

1

Source: Carbon Containment Lab

Registries:

administering the system

Registries are the formal administrators of the system. In today’s VCM, leading crediting programs such as Verra, Gold Standard, the American Carbon Registry, and the Climate Action Reserve set the methodologies and rules that determine which project types qualify and how rigorously impact must be demonstrated. Their associated registries then register eligible projects, issue credits once independent verification is complete, and maintain public records of all issuances, transfers, and retirements.

A new generation of registries is emerging alongside these incumbents. Isometric and oneshot.earth are building on the same core functions (methodology development, verification, public record-keeping) but with different design choices: faster methodology approval processes, and open data by default. In Isometric’s case, the business model also separates registry fees from credit sales to reduce potential conflicts of interest.

This is how a new infrastructure that is more transparent, rigorous and beneficial to project developers is emerging.

Independent rating agencies add a further layer of scrutiny. Firms like Calyx Global, BeZero, and Sylvera assess the integrity and risk profile of individual projects and methodologies across dimensions including additionality, permanence, leakage, and measurement robustness. Rather than issuing a binary pass/fail judgment, they provide a spectrum of quality assessment—from AAA down to D—that allows buyers to make informed decisions based on their own risk tolerance and budget.

Superpollutant projects are well-suited for high ratings. They tend to score well against the core criteria that the carbon market uses to determine integrity: measurability, additionality, and permanence. Learn more about these criteria in the quality section below.

“Credit quality should come from consensus: academics, industry experts, rating agencies, insurers, sophisticated buyers all agreeing on what the highest integrity methodology looks like. That’s a robust system, and frankly, it's the only kind of system that will earn lasting trust in carbon markets.’’

Thomas Annicq

Co-founder, oneshot.earth

The landscape of project developers

Below are examples of project developers operating in this space. We provide deeper dives into these companies in the next pages.

Mitti Labs

Agricultural methane

Implements Climate-smart rice farming techniques that reduce methane emission by 50%.

Vaulted Deep

Waste methane

Injects organic waste — which would otherwise release CO2 and methane into the atmosphere — underground for permanent storage.

Orizon

Waste methane

Captures methane emissions from biogas plants powered by waste.

ClimateWells

Oil & gas methane

Addresses emissions from aging oil and gas infrastructure.

Tradewater

Refrigerants / HFCs & methane

Collects and destroys refrigerants and halocarbons. Plugs methane leaks from orphaned oil & gas wells.

Recoolit

Refrigerants / HFCs

Recovers and destroys refrigerant gases from end-of-life air conditioners and cooling equipment.

ClimeCo

Nitrous oxide

Deploys efficient technology to reduce smokestacks at nylon and fertilizer factories.

"By tackling the most potent superpollutants, Tradewater has permanently eliminated the equivalent of over 11.3 million metric tons of CO₂, preventing them from being released in the atmosphere."

Year founded

2016

Country

USA (Headquarters: Chicago, Illinois)

Project type

ODS destruction & methane mitigation

Tradewater identifies, collects, and destroys haocarbons like ozone-depleting old refrigerants before they can leak into the atmosphere. Additionally, the company permanently prevents methane emissions by identifying and plugging actively leaking orphaned oil and gas wells.

Who buys their credits?

Tradewater has engaged with a wide range of customers in the voluntary and compliance carbon markets. These include large technology companies like Workday, leading universities (e.g., Duke University, Brown University), small companies (Schilling Cider, Planet FWD, and individuals via its e-commerce platform.

Volumes of credits issued

Tradewater has already eliminated more than 11.3 million tons CO₂e through over 100 completed projects in 7 countries, and expect to prevent emissions of at least 30 million tons by 2030.

“We plug aging wells in neighborhoods, near schools, and on croplands—stopping emissions at the source, protecting health, creating jobs, and restoring communities.”

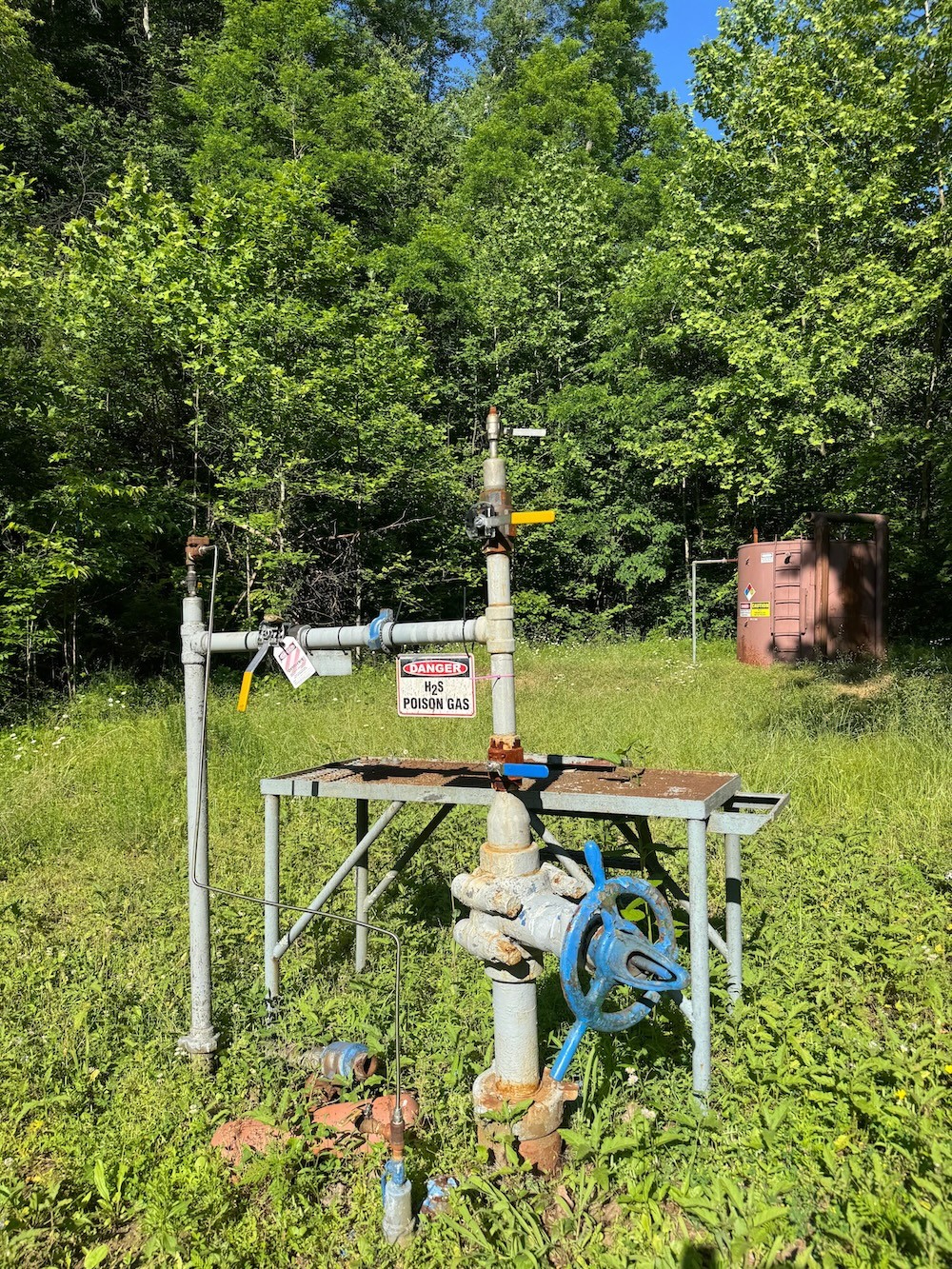

Year founded

2021

Country

USA (Headquarters: Austin, Texas)

Project type

Early decommissioning of oil and gas

ClimateWells accelerates the permanent closure of low-producing, high-emitting wells, stopping methane emissions at the source rather than decades later.

Who buys their credits?

Chubb, JPMorganChase

Note: Companies seeking high-integrity, immediate solutions can build projects or purchase credits from projects in their backyard.

Volumes of credits issued

70,000 with additional volume in development

Note: ClimateWells projects have received A-ratings from BeZero, representing high-quality, US-based projects.

“Advances in Digital Monitoring, Reporting and Verification allow us to monitor shifts in irrigation practices at the individual field level, with country-level scale. Once practices have shifted, the reduction in methane emissions is permanent and has near-term positive climate impact.''

Year founded

2023

Country

United States & India

Project type

Agricultural Methane (Rice)

Mitti Labs works with smallholder farmers to implement techniques (like Alternate Wetting and Drying) that reduce methane emissions from rice paddies by 50% and cut water consumption by 40%.

Who buys their credits?

Cool Effect

Note: Mitti Labs is the first project developer worldwide to have issued Tier 3 credits for rice methane reduction.

Volumes of credits issued

First issuance in April 2026

By 2028, Mitti Labs plans to scale its issuance of methane-based credits to 2 Mn credits per year.

“Recoolit has pioneered a scalable and transparent approach to solving 3 gigatonnes of yearly global refrigerant emissions. The carbon market, and buyers who are willing to support high-quality and catalytic projects, are critical to helping our solution scale.”

Year founded

2023

Country

United States & Indonesia

Project type

Refrigerant Recovery

Recoolit recovers and destroys refrigerant gases from end-of-life air conditioners and cooling equipment in emerging markets (starting with Indonesia).

Who buys their credits?

Google

Note: Google signed a multi-year deal to purchase 250,000 credits.

Volumes of credits issued

~250,000+ (Committed/Issued).

Note: Early pilot batches were small (~1,400 tonnes), but the Google partnership has scaled their validatable volume significantly.

Scale and integrity

The superpollutant credit market is active, growing, and beginning to show meaningful signals around scale and integrity. But to understand where it is headed, it helps to understand where it stands.

Volumes:

gaining momentum

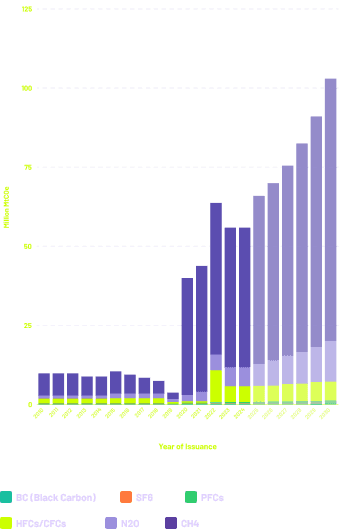

Methane credit retirements reached a new high in 2025, with 19.4 million tonnes CO₂e retired — a 128% increase from 2015 levels, and a near-doubling from 2020 alone.

Yet the overall picture, while encouraging, needs context. Since 2015, the VCM has addressed roughly 420 million tonnes of superpollutant emissions in total.

That is less than 3% of the approximately 15 billion tonnes of superpollutants emitted globally every year. The market is growing, but it has not yet approached its potential.

Projections from the CC Lab suggest that, under business-as-usual (BAU) growth, cumulative mitigation via the VCM reached one billion tonnes in 2023.

Under a more aggressive investment scenario, 3.5 billion tonnes CO₂e is within reach. The gap between those two scenarios is largely a function of demand.

“There are a lot of high-quality, methane-reduction credits available, partly because we're creating more waste but also because of carbon funding. We have been working with a number of projects to use the revenue from credit sales to improve technology, close leaks and create even more reductions by adding additional tools such as composting and biomethane. We're starting to catalyze these kinds of investments towards scale.'’

Jodi Manning

CEO, Cool Effect

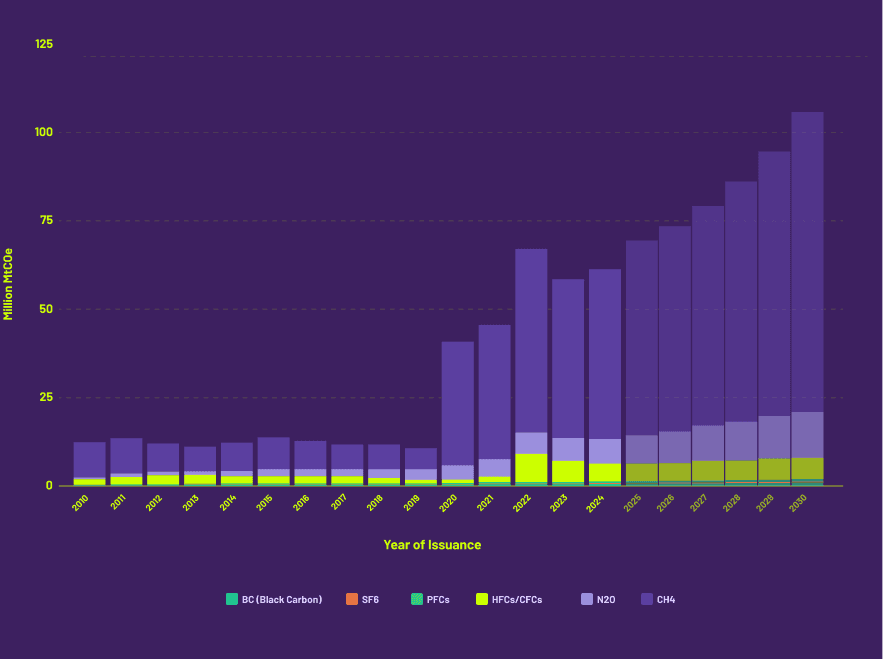

Total credits issued by gases under BaU growth scenario

Price:

the value hiding in plain sight

Targeted superpollutant measures have the capacity to deliver four times the net climate benefit of equivalent CO₂ reductions by 2050. That means every dollar invested in superpollutant abatement generates four times the environmental return of the same dollar spent on CO₂ reduction alone. The market has not yet priced this in.

For more on this, read Tradewater’s “Targeting Super Pollutants: The Fastest Path to Climate Imact.”

Many high-quality superpollutant credits trade at prices well below carbon-focused credits, even when their near-term warming impact is substantially greater. Superpollutant avoidance projects typically trade in the range of $10–$20 per tonne of CO₂-equivalent on average, depending on project type.

Durable removal credits — biochar, enhanced weathering, direct air capture — average $187 to $349 per tonne or higher, according to 2025 market data. For buyers evaluating cost per unit of climate benefit, this creates a striking value proposition.

Cool Effect calculates that over 300 million tonnes of CO₂-equivalent from superpollutants could be mitigated by 2030 through existing project types alone — if market demand in the VCM materializes.

“These are the ugly ducklings. Nobody says 'I want to support a manure lagoon.' But they punch above their weight. They are under-appreciated and undervalued. They are the low hanging fruit of emission mitigation.’’

Donna Lee

Co-founder, Calyx Global

The high-integrity side of the market: where superpollutants dominate

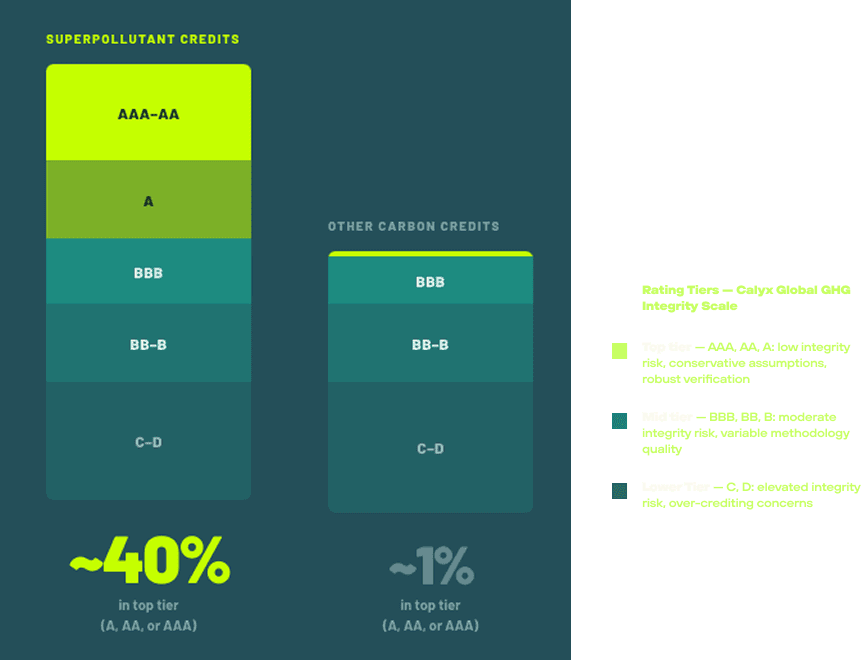

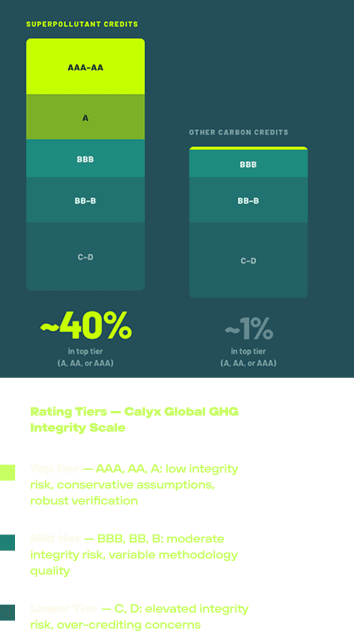

Of more than 1,000 carbon credits rated by Calyx Global, roughly 40% of superpollutant credits achieve a top-tier rating (AAA, AA, or A). For non-superpollutant credits, that figure is just 1%.

Source: Calyx Global

Quality:

where superpollutants outperform

Of the more than 1,000 carbon credits rated by Calyx Global, approximately 40% of superpollutant credits fall into the top tier — AAA, AA, or A — compared to just 1% of non-superpollutant credits. Superpollutant projects dominate the highest-quality end of the market. That said, quality is not uniform across the category.

Superpollutant projects score well on the three criteria that define carbon credit quality. Measurability is high because abatement involves a specific, bounded process — a refrigerant destroyed, a well plugged — that can be directly quantified.

Additionality tends to be strong because many of these activities, such as refrigerant destruction, have no commercial value without a credit incentive. And permanence is, in many cases, absolute — when a superpollutant is destroyed, there is nothing to reverse. The gas is gone.

This structural advantage is part of what makes superpollutant credits an increasingly compelling option for buyers who want high-quality climate action at accessible price points.

Over half of superpollutant credits still fall below the top tier, and the history of the market includes episodes — most notably the HFC-23 scandal of the early CDM era, where some manufacturers created refrigerants specifically to sell credits for destroying them — that left lasting reputational damage.

The market has learned from those episodes. Methodologies have been revised, oversight has strengthened, and the second generation of superpollutant credits is more robust than the first. The direction of travel is clear.

The infrastructure for high-quality superpollutant mitigation exists, is improving, and is already producing credits that outperform the broader market.

"These processes where you're capturing the methane, you're destroying the HFC — they're non-reversible. That is the pure definition of permanence."

Jodi Manning

CEO, Cool Effect

"You've got to address one of the elephants in the room, which is methane. These orphaned oil wells are not going to be plugged absent of creating some form of carbon credit. This is an emergency brake on climate."

Erik Hansen

Chief Sustainability Officer, Workday

“In addition to reducing pollution, the decommissioning process positively impacts communities by creating local job opportunities, particularly for former oil and gas industry employees, and helps reduce the health impact to local communities from industrial emissions.’’

"Our partnerships with Recoolit and Cool Effect are focused on eliminating more than 25,000 tons of superpollutants by 2030 — aiming to prevent warming roughly equivalent to 1 million tons of CO2 in the long-term (and, given their potency, 3 million tons in the short-term).’’

Google Company News, May 2025

Timeline: the superpollutant trade (2015–2025)

Scaling climate solutions for

near-term impact

03 | Scaling climate solutions for near-term impact

Registry innovation: accelerating speed to market

One of the most significant bottlenecks in scaling superpollutant projects has been the slow pace of methodology development and approval. Traditional registry processes have taken up to four years to bring new methodologies to market — an unacceptable timeline given the urgency of climate action.

New registry models are emerging to address this constraint. The Open Carbon Protocol, developed by oneshot.earth, has pioneered an approach designed for speed without compromising integrity. By leveraging the peer review process of academic journals to establish scientific consensus, the protocol can move methodologies from submission to live status in seven to eight months — a dramatic improvement over legacy timelines.

The Open Carbon Protocol currently supports three methodologies for tackling superpollutants: plugging marginal and orphaned oil and gas wells, and destroying HFCs. Six more are in development, including two focused on agricultural methane abatement. HFC Destruction in Article 5 countries, which the Carbon Containment Lab proposed, is in final review. This acceleration in methodology development creates new opportunities for project developers who have been waiting on the sidelines.

Building trust from the ground up

Isometric was founded to restore trust in carbon markets. Its buyer-pays model fixed the fundamental conflict of interest in legacy registries, where registries were paid by the project developers whose credits they verify. And by publishing the underlying data behind every credit — calculations, evidence, and life cycle assessments — on the Isometric Registry, they’re enabling the science to speak for itself.

Isometric also transformed certification by solving the cash flow gaps created by annual credit issuance. Certify’s AI-assisted validation and automated data submission remove the manual bottlenecks that have slowed developers down, delivering monthly credit issuance that unlocks the path to scale.

In 2025, Isometric expanded beyond carbon removal to superpollutant reduction — spanning methane to refrigerants — bringing the same transparency, speed, and aligned incentives that have defined its approach to carbon removal.

“Buyers don't need to trust Isometric. They can trust the data."

Eamon Jubbawy

CEO, Isometric

Accounting for short-lived emissions

“We need updated rules of the game to incentivize action.”

Hara Wang

Co-founder and Chief Programs Officer, Cascade

All greenhouse gases are currently translated into a single common unit: carbon dioxide equivalent, or CO₂e. This relies on global warming potential metrics, typically measured over 100 years.

But superpollutants do not behave like carbon dioxide. Their warming impact is intense and front-loaded. Measuring them over a 100-year horizon — the GWP100 standard — obscures this.

Scientists and economists are actively working on alternatives. Some advocate for GWP20 as a more honest lens for short-lived gases. The Global Heat Reduction Initiative promotes what they say is a more holistic form of carbon accounting, expanding traditional emissions accounting to include different timescales. Others are developing new impact frameworks — like the GWP* metric — that attempt to better capture the time-temperature dynamics of different pollutants.

Carbon Direct names the practical implication directly: instead of exclusively following a GWP100 accounting approach, buyers should assess the actual avoided warming from superpollutant projects on an annual basis to achieve the most rigorous measurement of planet cooling across multiple timescales.

While those debates unfold, emissions continue.

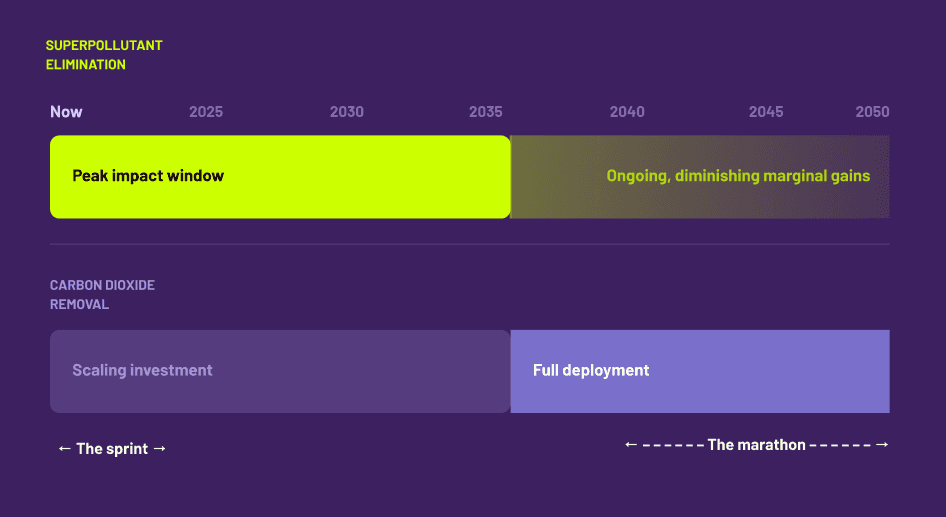

The sprint and the marathon

A complete climate strategy requires two timeframes. Superpollutant elimination delivers fast, measurable near-term cooling. Carbon dioxide removal builds the structural foundation for long-term stability. Both are necessary. Neither is sufficient alone.

Portfolio architecture

The “sprint” to 2030 requires rapid reductions in short-lived climate pollutants. The “marathon” to mid-century requires structural decarbonization and durable carbon removals. A climate strategy that addresses only one of these dimensions is, by definition, incomplete.

Pairing superpollutant mitigation with durable carbon removal — an approach Carbon Direct calls CDR pairing — ensures that near-term cooling doesn't come at the expense of long-term carbon balance. The result is a portfolio that drives sustained climate impact across both timeframes.

Rather than asking whether methane avoidance is “better” than carbon removals, buyers are allocating capital across both.

The idea of time-matched replacement is emerging as one organizing principle. Methane remains in the atmosphere for roughly 12 years. Some buyers are pairing methane mitigation today with longer-lived carbon removal commitments over time, ensuring that near-term cooling does not undermine long-term carbon balance.

Read “Bridging the Time Gap: What “Durability” Means for Carbon Removal in Farm Landscapes” for more on this concept.

This approach is still evolving. There are active debates about “like-for-like” accounting versus portfolio blending models. Some argue that companies should neutralize emissions gas-by-gas. Others believe diversified climate portfolios better reflect physical reality and capital efficiency.

Credible actors are already experimenting with structured combinations. The question is no longer whether superpollutants belong in corporate climate strategies, but how they are integrated.

Technology for impact

Cheaper technology, better data: a market that’s easier to trust

Methane and refrigerant emissions have historically been difficult to measure precisely. That is changing fast.

A new generation of satellite and sensor technology is bringing the cost of emissions monitoring down sharply and the accuracy up. MethaneSAT, launched in 2024, can detect methane emissions at the facility level across entire oil and gas basins. Carbon Mapper, a partnership between Planet, NASA's Jet Propulsion Laboratory, and a coalition of state and philanthropic funders, can pinpoint individual point-source emitters — a leaking pipeline, a specific landfill cell — from orbit. The price of deploying this kind of monitoring has fallen substantially over the past decade.

Cheaper and more precise dMRV (digital measurement, reporting and verification) lowers the cost of developing new methodologies. It makes verification faster and more defensible. And it opens up project types that were previously too expensive to monitor at the required level of precision. The infrastructure for high-quality superpollutant credits is getting better and cheaper at the same time.

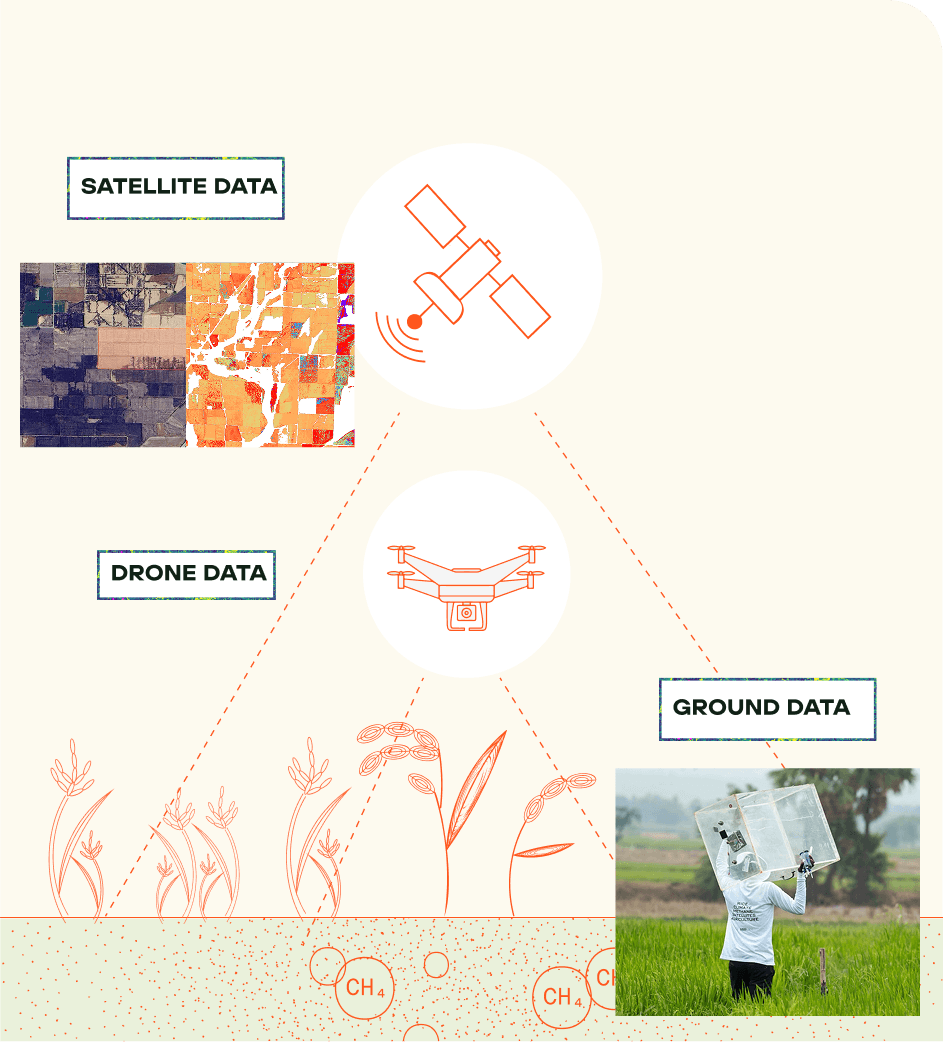

Monitoring emissions from rice farming via satellite: the Mitti Labs example

Mitti Labs uses remote sensing and GIS to analyze agriculture at scale across entire regions — without visiting individual fields. Drawing on data from satellites, aircraft, and drones, they capture insights at varying levels of detail and coverage to serve farmers, researchers, and carbon credit buyers.

A key strength is their use of microwave remote sensing, particularly L-band radar, which can penetrate clouds, vegetation, and shallow soil — making it especially valuable during India's monsoon season.

Combined with optical and thermal sensors, this allows them to monitor crop health, soil moisture, flooding, and irrigation patterns with high accuracy.

Their GIS pipelines transform raw satellite data into practical products: crop calendars, field condition analyses, and practice inference tools. These support real-world decisions around irrigation investment, Climate-smart agriculture compliance, and carbon credit verification.

Public support

Ultimately, the industries that generate superpollutants must be part of the solution. Whether through voluntary commitments, sectoral agreements, or regulatory requirements, oil and gas companies, agricultural producers, and industrial manufacturers need incentives — or mandates — to invest in abatement.

The demand that will take superpollutant abatement to the scale and time horizons the climate requires is not going to come from big tech buyers alone. It will come from industry and government. Building toward that handoff — in financial products, in policy frameworks, in procurement infrastructure — is the work of the next five years.

“We believe that the work we are doing in the VCM is a way to chart the initial path forward. Our methane reduction programs in rice farming can reach a larger scale faster with support of local and central governments.”

Devdut Dalal

Co-founder, Mitti Labs

Demand expansion

A small cohort of climate leaders including Google, Netflix, and Workday have integrated superpollutant elimination into their climate portfolios. Their purchases have helped to validate the market.

In March 2026, Google pledged $50 million toward superpollutant elimination through 2030. The announcement came as part of the launch of the Superpollutant Action Initiative, a coalition of corporate buyers with the aim to deploy $100 million through 2030 to unlock action in areas where progress is critically needed.

A “Corporate Roadmap for Superpollutant Action” will be a central product of this coalition and will be released in September 2026 at NY Climate Week. In partnership with the Carbon Containment Lab and guided by a committee of leading scientists, policy experts, and economists, this roadmap will guide companies on creating near-term climate impact through carbon markets, value-chain interventions, and policy engagement.

"Action this decade can limit peak warming by up to 0.1°C, buying critical time for long-term decarbonization, protecting communities, and reducing the risk of dangerous climate feedbacks. By aggressively cutting superpollutant emissions, we can avoid more than 0.5°C of warming by 2050. ''

Superpollutant Action Initiative

Launched March 2026

The permission problem: beyond the early adopters

Corporate buyers face a barrage of conflicting guidance: Can they use credits for ongoing emissions or only residual emissions? Should they prioritize removals over reductions? What counts toward science-based targets? How should they treat superpollutants that decay over time versus permanent CO₂ removals?

Organizations like the Science Based Targets initiative (SBTi) and the Voluntary Carbon Markets Integrity Initiative (VCMI) have attempted to provide clarity, often adding complexity in the process. Emerging approaches point toward a progressive transition from short-lived abatement credits to more durable removals, but without a clearer roadmap, companies are left with commercial and accounting questions they don't know how to answer.

Clearer guidance matters. Companies need actionable rules of engagement. Reducing buyer hesitation will require aligning norms with physics: short-lived gases drive near-term warming, and addressing them delivers measurable climate benefit within years. When claims frameworks reflect that reality, demand can expand beyond early adopters.

"Compared to emerging technologies like carbon dioxide removal (CDR), super pollutant credits are often more cost-effective while delivering significant climate benefits in the near term. This makes them an attractive option for organizations looking to meet immediate decarbonization goals.’’

Rubicon Carbon: How Super Pollutant Credits Abate the Most Potent Greenhouse Gases

Creating easy buttons for the mid-market

Mid-market buyers need simplified procurement pathways that don't require building internal expertise from scratch.

This is where the portfolio products, aggregated procurement platforms, and intermediaries described in previous sections do their most important work — not just for risk management, but for accessibility.

Transparent ratings, standardized due diligence, clear pricing, and simplified onboarding reduce the transaction friction that keeps cautious buyers out of the market entirely.

From niche to necessary

Superpollutants are responsible for nearly half of current warming. They can be mitigated with affordable, available technologies. Each dollar invested in their abatement delivers more than four times the near-term climate benefit of a dollar invested in CO₂ reductions alone.

The case for scaling superpollutant abatement is overwhelming. The VCM has proven it can test innovations, establish methodologies, and catalyze early action. Now it must evolve to drive transformation at scale.

Annual retirements of methane credits have tripled since 2019. Project developers are scaling capacity. Portfolio products are lowering the barrier to entry. But the gap between what the market is doing and what the climate requires is still vast. Closing it will require deliberate acceleration across every lever available.

In five years, a bold but believable future might feature headlines like: "75% of Fortune 500 Companies Make Carbon Neutral Claims" or "Tax Credits for Superpollutants Unlock Billions in Mitigation Investment" or even "Project Developers Struggle to Find Remaining Refrigerants as Market Clears Supply."

Those outcomes are achievable — but only if stakeholders across the ecosystem recognize that addressing superpollutants is not a distraction from decarbonization but a critical complement to it. The 2020s can be the decade the world finally got serious about the pollutants responsible for half of global warming. The tools exist. The moment is now.

Selected resources for readers who want to go further

Title

Publisher

ClimateWells & partners

Climate Analytics

Climate Impact X

Yale School of Management

Climate & Clean Air Coalition

Lauren Singer & Nick van Odsol